For many reasons, I urge my clients to look at home equity as "separate" from the other assets in their retirement savings strategy. Since 2008, many of us have learned that real estate, particularly the value of our homes, may not be a dependable resource to tap. Home equity should be set aside and, essentially, parked during retirement. The over-use of reverse mortgages, second mortgages and home equity lines of credit in retirement have gotten many into financial trouble in recent years -- and can undermine a retirement plan. We want our homes to be our creature comforts in retirement and provide peace of mind. For most Americans, that means the family residence should not be considered a primary retirement investment. Additionally, real estate "flipping" is no longer a tool to jump start a quick and easy nest egg.

|

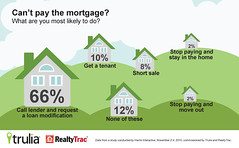

| (Photo credit: truliavisuals) |

Here are three simple tips to help position you for a mortgage-free retirement.

1. Don't take on more home debt than you can comfortably afford. If we learned anything from the recent past, it is the risks of taking on too much mortgage debt. If your monthly mortgage payments leave no financial cushion or ability to save towards retirement, it's best to reassess your plan. Generally, mortgage expenses should be no more than 28 percent of your monthly budget. Be particularly careful with adjustable-rate mortgages, which may begin with a lower, manageable interest rate that rises over time and may be "interest only" for a number of years, meaning that none of your monthly payments will be applied to your outstanding balance.

2. Balance paying off your home mortgage with your retirement savings. You have a limited pot of money to draw from on a monthly basis, and many different financial priorities. Make sure that retirement savings are a priority in your monthly budget and do not get squeezed out by other expenses. Postponing retirement savings has a number of drawbacks. First, your money does not have as much time to grow. To illustrate this, one person starts contributing $100 per month towards a retirement plan at age 21 and, assuming a 6 percent interest rate, at age 65 has $258,426 in that plan. Assuming the same interest rate, another person who doesn't start saving until age 40 would need to put $372 per month into their retirement plan to end up with the same amount of money at age 65. The second drawback is you may be walking away from "free money" if your employer offers an employer-match program. Many employers encourage you to save for retirement by offering match programs and other conveniences such as automatic payroll deduction.

3. Consider increasing your monthly mortgage payments. Opting for an accelerated payment schedule on your mortgage can take years off your mortgage. Paying your loan off more quickly means that you could retire mortgage-free, bringing more financial flexibility and less stress in retirement. And who doesn't want a stress-free retirement? Many lenders offer programs that let you bifurcate monthly payments into two smaller installments per month. This means you pay the same total monthly amount, but chip away at principal more quickly. Over 15, 20 and 30 years, this can result in significant savings.

Unfortunately, with the retraction of the real estate market in recent years, over-inflated properties in many regions have lost value, mortgages have gone underwater and, in the worst of cases, people have lost their homes. Due to this turmoil, our perspective on home ownership -- as part of a long-term retirement strategy -- is normalizing. Our economy is slowly getting back to a more rational approach to real estate.

With this in mind, retirees can view their home more realistically -- first and foremost as a place to live, and second as a more flexible but less critical asset to help deliver the retirement they desire.

ING Retirement Coach Jacob Gold is a third generation financial advisor. He is a published author of Financial Intelligence; Getting Back to Basics after an Economic Meltdown, which was published in August 2009. Gold is a Certified Financial Planner™ practitioner and FINRA series seven, 24 and 66 securities registered.

Securities and Investment advisory services offered through ING Financial Partners, Member SIPC. Neither ING Financial Partners nor its representatives offer tax advice.

By Jacob Gold, ING retirement coach, author

Taken from: http://www.huffingtonpost.com/jacob-gold/mortgage-free-retirement_b_1968286.html

No comments:

Post a Comment