|

| One Wells Fargo Center – Charlotte, North Carolina, will succeed as Headquarters for East Coast Operations of Wells Fargo (Photo credit: Wikipedia) |

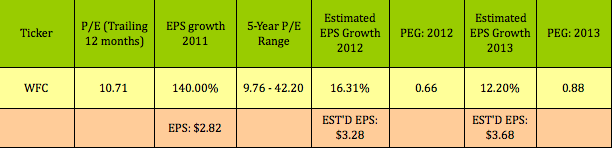

WFC actually looks undervalued on a Price-to-Earnings-Growth, PEG basis, with projected growth of over 16% in 2012, and over 12% in 2013:

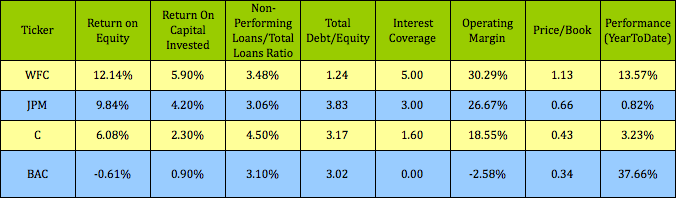

Here's how WFC stacks up vs. the 3 other biggest US banks - JP Morgan Chase, (JPM), Citigroup, (C), and Bank of America, (BAC). WFC leads the pack in return on equity, return on capital invested, operating margin, interest coverage, and has the lowest debt/equity.

The picture isn't totally perfect at WFC, which has a ratio of 3.48% on its non-performing loans, second only to Citigroup in the big 4 group. The overall industry avg. appears to be approximately 2.28%, but given the differences in which loans are listed and which aren't, this figure may be higher. The loan ratios shown below also don't include loans guaranteed by guess who? You and I, the ever-generous US taxpayer, via various US government agencies.

WFC has been given a higher price/book by the market, which has also pushed its shares up 13.57% as of 6/7/12. Oddly, Bank of America, which has the lowest scores on many of these metrics, has outperformed the entire group so far in 2012, on a roller coaster ride from $5.56 at the start of the year, up to $9.93 in late March, back down to $7.42 this week. WFC has a much lower beta of 1.34, vs. BAC's volatile 2.32.

Share Performance: Although BAC has outperformed the rest of the big 4, WFC has been the steadiest performer year-to-date, with a much smaller draw-down than the other 3 stocks during the spring pullback:

(Above chart source: YahooFinance.com)

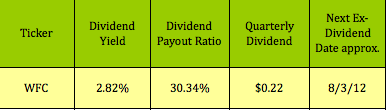

Dividends: WFC made a huge 83% increase in its dividend payouts in the second quarter of 2012, increasing them to $.22/quarter, from $.12. Citigroup and Bank of America are still only only able to pay $.01/quarter, due to ongoing bailout capital restrictions.

Like WFC, JPM got the go-ahead to increase its dividends again in 2011, and has increased them from $.25 to $.30/quarter in 2012. However, with its looming trading loss scandal, some analysts are questioning if there will be any more JPM dividend raises in the near future. After its shares got whacked nearly 33%, JPM now has the highest dividend yield, (over 3.6%), in the group.

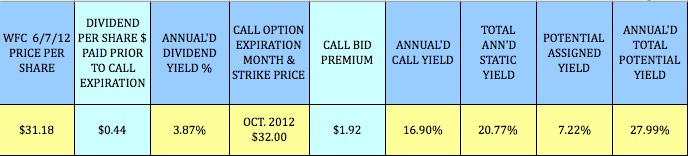

Covered Calls: WFC has some fairly high options yields, which will allow you to increase its dividend yield substantially. In addition, the additional option income will also serve to lessen the risk. (We list more details for this and many other trades in our Covered Call Table.)

If you want to be even more conservative, you might consider selling cash secured puts on WFC, below its current share price. The Jan. 2013 $30.00 put option offers a $2.91 payout, vs. the $.44 in dividend payouts between now and Jan. 2013.

(You can see more details for this and many other put option trades in our Cash Secured Put Table.)

No comments:

Post a Comment